Hidden Treasures: Undervalued Stocks with Massive Upside

#1 Trades at Half of Book Value and management is buying back 6% of the shares outstanding, #2 5X Cashflow and 7.8% Dividend Yield, #3 Single digit P/E, .80X Book Value, stock buybacks and dividends.

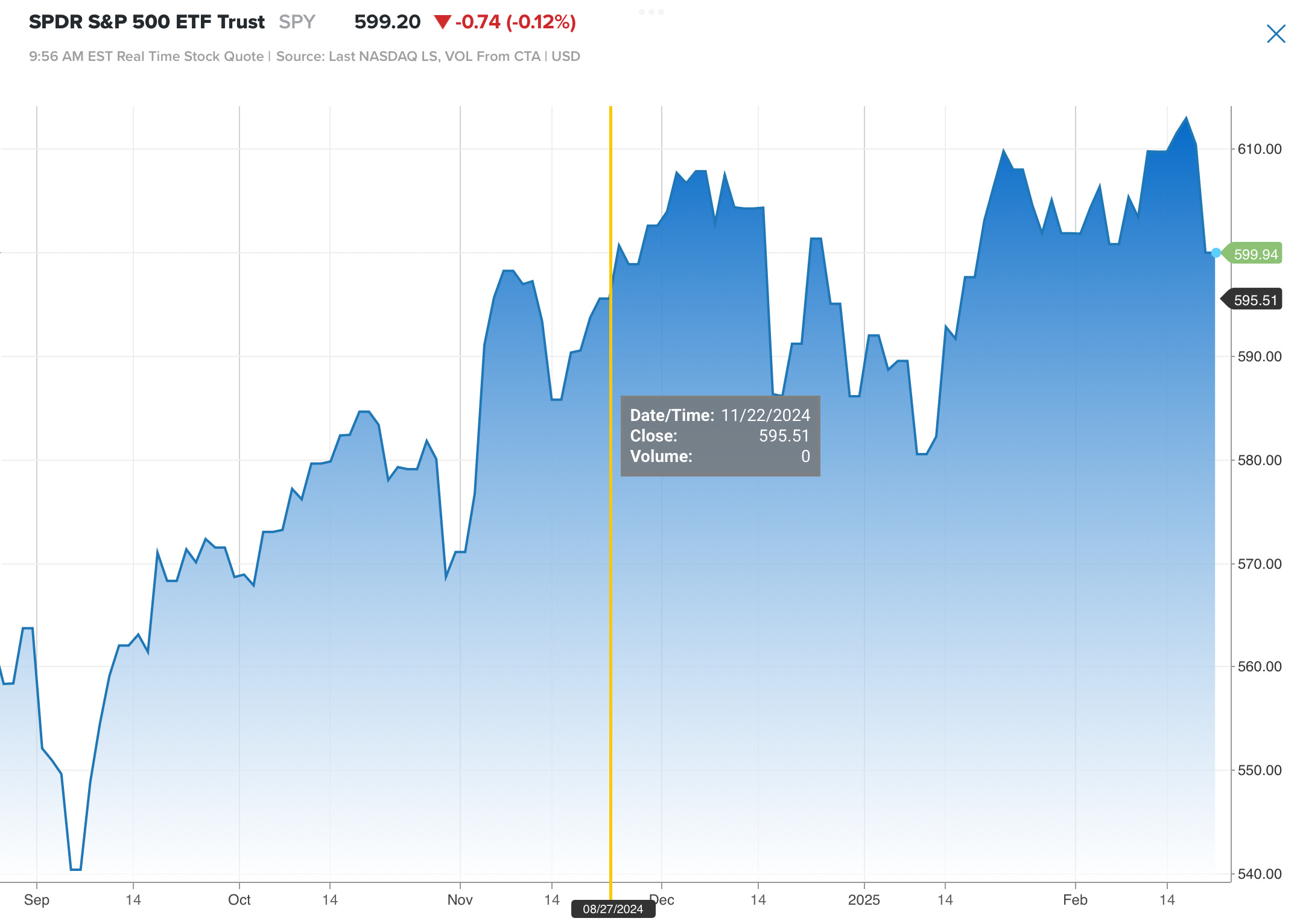

Market Overview:

Multiple days of institutional selling. Caution is warranted

Legal

Recent Recommendations

Arcelor Mittal $ MT

ArcelorMittal S.A., together with its subsidiaries, operates as integrated steel and mining companies in the United States, Europe, and internationally. It offers semi-finished flat products, including slabs; finished flat products comprising plates, hot- and cold-rolled coils and sheets, hot-dipped and electro-galvanized coils and sheets, tinplate, and color coated coils and sheets; semi-finished long products, such as blooms and billets; finished long products consisting of bars, wire-rods, structural sections, rails, sheet piles, and wire-products; and seamless and welded pipes and tubes.

The company also provides mining products, such as iron ore lumps, fines, concentrates, pellets, and sinter feeds; and coking coal. It sells its products to various customers in the automotive, appliance, engineering, construction, energy, and machinery industries through a centralized marketing organization, as well as distributors. The company has iron ore mining activities in Brazil, Bosnia, Canada, Liberia, Mexico, South Africa, and Ukraine. ArcelorMittal S.A. was founded in 1976 and is headquartered in Luxembourg City, Luxembourg.

Global Steel Industry Overview

The steel industry is cyclical and closely tied to global economic growth, infrastructure spending, and industrial production. China dominates global steel production, accounting for over half of the world’s output, which impacts global pricing and trade policies. Environmental regulations, carbon emissions reduction targets, and demand for greener steel are reshaping the industry’s landscape.

Competitive Landscape

ArcelorMittal competes with major global steelmakers like China Baowu Steel, Nippon Steel, and POSCO. It has a significant advantage in its vertically integrated operations, strong R&D investment, and geographic diversification.

Key Takeaways

• ArcelorMittal remains the largest global steel producer but faces competition from Nucor and Cleveland-Cliffs in North America, both of which focus more on domestic markets.

• Nucor is the most profitable per ton due to its high-margin product mix, while POSCO has a strong balance sheet and consistent dividends.

• Cleveland-Cliffs has higher debt due to acquisitions but is expanding in the automotive steel market.

• ArcelorMittal has significant global exposure and is investing heavily in electric arc furnaces for low-carbon steel production.

Incredible valuation: 6X Cash flow, half of book value, 30% growth, and management is committed to buying back stock.

Stock Buybacks:

Reducing shares outstanding by 6%

Keep reading with a 7-day free trial

Subscribe to Stock Gems to keep reading this post and get 7 days of free access to the full post archives.